The Great Middle-Class Squeeze: How India’s Tax Regime Punishes the Honest While the Powerful Walk Free

Income tax, GST, LTCG, STCG, property tax, cess upon cess — the salaried Indian is taxed at every breath. Foreign investors are fleeing at record speed, the rupee has crashed 7% in five months to touch INR 97, and the only winners in this economy are the netas, babus, and cronies who designed the system in the first place.

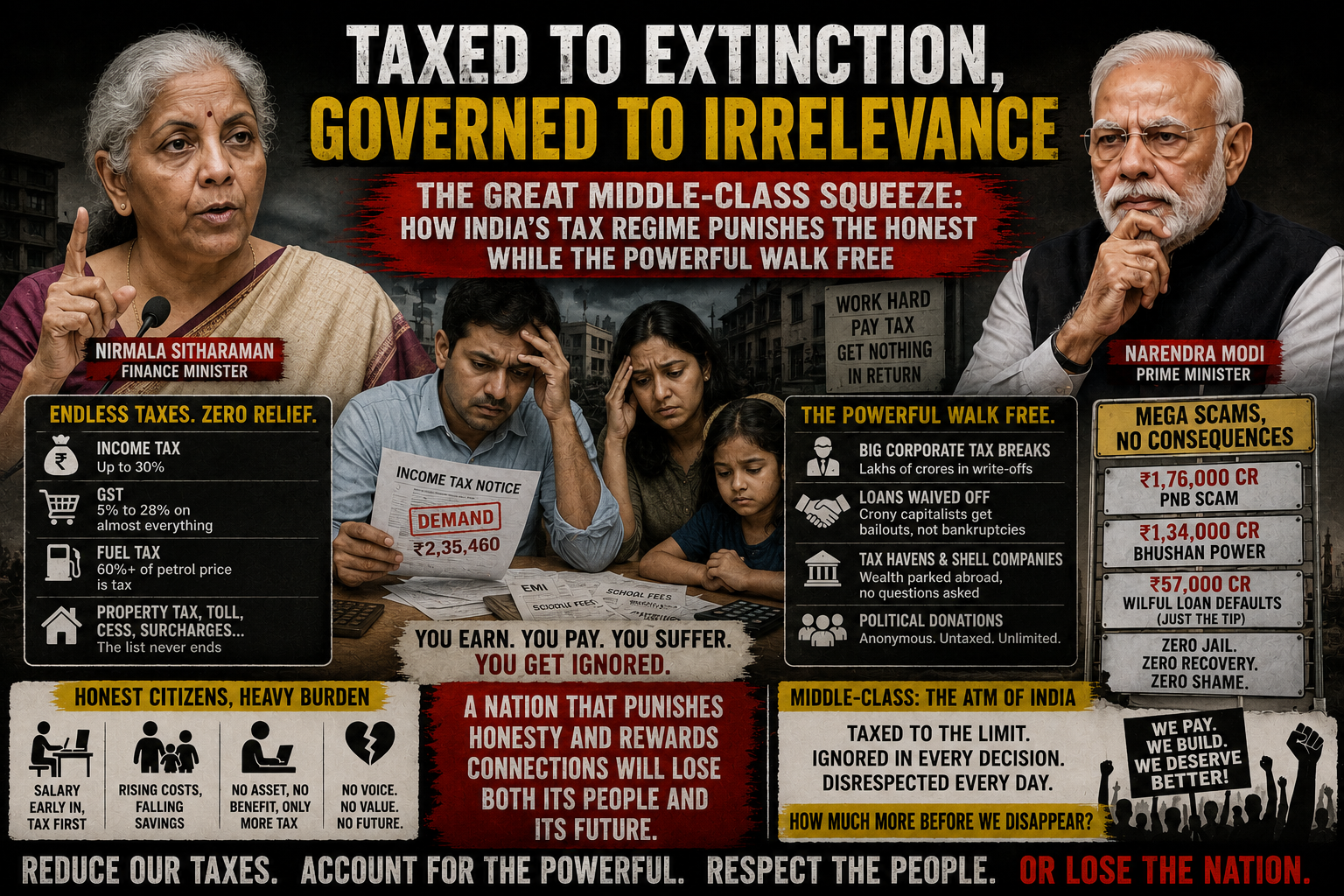

Here is what it means to be an honest, salaried, middle-class Indian in 2026. You earn your income — every rupee of it documented, every rupee visible to the taxman, every rupee deducted at source before it reaches your bank account. You pay income tax at rates up to 30 per cent. On the money that remains, you spend — and pay 5 per cent GST on essentials, 18 per cent on most goods and services, and 28 per cent on anything the government deems a “luxury,” which increasingly includes things that middle-class families consider necessities. If you manage to save and invest, your gains are taxed again — 12.5 per cent on long-term capital gains, 20 per cent on short-term gains. The property you live in is taxed annually by your municipality. The fuel you put in your car carries excise duties, cesses, and VAT that add up to over 50 per cent of the pump price. Your insurance premiums were taxed at 18 per cent GST until recent reforms. Even your death is not tax-free — your heirs will pay stamp duty, registration fees, and capital gains on anything they inherit and later sell.

Now here is what it means to be powerful in India. If you are a politician, your electoral income is untraceable, your assets grow inexplicably from election to election, and your agricultural income — however implausible — is tax-free. If you are a senior bureaucrat, your pension is generous, your perquisites untaxed, and your post-retirement consultancies structured to minimise liability. If you are a billionaire industrialist, your companies enjoy tax holidays, your losses are carried forward across years to offset gains, your holding structures are routed through Singapore and Mauritius, and your effective tax rate — as multiple analyses have shown — is a fraction of what a salaried software engineer in Bengaluru pays. And if you are a wealthy farmer — owning hundreds of acres, earning crores from agribusiness, real estate laundered as “agricultural land,” and commodity trading — you pay zero income tax, because in India, all agricultural income is exempt, regardless of scale.

This is not a tax system. It is a caste system of taxation — where your position in the hierarchy determines not how much you contribute but how much you can escape.

I. The Taxation Labyrinth: How Many Times Can You Tax the Same Rupee?

Income Tax → GST → Capital Gains → Property Tax → Cess → Surcharge → Stamp Duty → RepeatThe fundamental injustice of India’s tax architecture is not the rate at any single point — it is the cumulative, compounding, multi-layered extraction that follows a single rupee as it moves through the life of an honest taxpayer. Consider the journey of INR 100 earned by a salaried professional.

First, income tax and surcharge reduce it. At the highest slab (above INR 15 lakh), the effective rate including cess and surcharge can exceed 30 per cent. So INR 100 becomes roughly INR 70. Of that INR 70, when spent on goods and services, GST takes another 18 per cent on average — leaving approximately INR 57 of actual purchasing power. If any of the remaining savings are invested in equities, the gains are taxed again: 12.5 per cent LTCG on gains exceeding INR 1.25 lakh after holding for a year, or 20 per cent STCG if sold within a year. The Securities Transaction Tax is levied on top of that. If the investment is in property, the buyer pays stamp duty (5–7 per cent in most states), registration fees, and ongoing annual property tax — and when the property is eventually sold, capital gains tax is levied again on the appreciation. At every stage, there is a cess: education cess, health cess, Swachh Bharat cess, infrastructure cess — cesses that are not shared with states and whose utilisation is rarely audited.

The result is that a salaried Indian earning INR 25 lakh per annum — solidly middle-class, not wealthy by any stretch — can end up surrendering 45–52 per cent of their gross income to various levels of government when all direct and indirect taxes are accounted for. This is a higher effective rate than many Scandinavian countries offer, but without the universal healthcare, world-class public education, or functioning social safety net that those tax rates fund. The Indian middle class pays European taxes and receives sub-Saharan services.

The Untouchables: Who Doesn’t Pay

Against this relentless extraction from the salaried class, consider who escapes the net entirely. All agricultural income is exempt from income tax under Section 10(1) of the Income Tax Act — a provision designed for subsistence farmers that has become a legal shield for agribusiness empires, land-owning politicians, and real estate operators who classify rental income from farmhouses as “agricultural income.” There is no income threshold for this exemption. A farmer earning INR 5 lakh and a farmer earning INR 5 crore enjoy the same zero tax rate. MPs and MLAs file affidavits showing their wealth doubling and tripling between elections, with the increase attributed to farming and “other sources” that conveniently fall outside the tax net. The salaried professional, meanwhile, cannot hide a single rupee — because TDS ensures the government takes its cut before the money even reaches them.

India’s corporate tax rate was slashed to 22 per cent (with an effective rate of about 25.17 per cent including surcharge and cess) in 2019, in what was presented as a “stimulus” for investment. New manufacturing companies pay an even lower effective rate of about 17 per cent. Meanwhile, the individual taxpayer earning INR 15 lakh — a fraction of what these corporations earn — pays a higher effective rate. The asymmetry is not accidental. It is structural. It reflects a political economy in which corporations fund elections, and salaried individuals merely fund the exchequer.

That question was asked on the floor of Parliament itself. Finance Minister Nirmala Sitharaman’s response was to cite India’s tax-to-GDP ratio of 18.4 per cent and call it “one of the lowest among comparable G20 developing economies.” This is a masterclass in deflection. The tax-to-GDP ratio is low precisely because the tax base is narrow — because agriculture, the informal sector, and politically connected wealth are exempt or escape the net. The burden falls disproportionately on the narrow band of compliant, salaried taxpayers. The ratio tells you nothing about the intensity of extraction from that band. A country where 3 per cent of the population pays 97 per cent of all income tax is not a low-tax country. It is a country that has chosen to crush a small, captive group while allowing everyone else to walk free.

II. Foreign Capital in Retreat: INR 2 Lakh Crore Gone in Four Months

The Worst FII Exodus Since 1993 — and It’s Not Just About Global FactorsIf the tax regime punishes domestic savers, it has also driven a historic exodus of foreign capital. In the first four months of 2026, foreign portfolio investors pulled out over INR 2 lakh crore from Indian equities — a number that has already exceeded the total FII outflow for the entirety of 2025 (INR 1.66 lakh crore) and the entirety of 2024 (INR 1.29 lakh crore). According to a JM Financial report, aggregate foreign holding in Indian listed stocks has fallen to a 14-year low of 14.7 per cent. This is the worst sustained foreign selling since FPI investing in Indian equities was first permitted in 1993.

The government and its defenders attribute this entirely to global factors — rising US bond yields, the West Asia conflict, crude above $100. These are real factors. But they are not the full picture. Taiwan’s stock market has surged nearly 40 per cent in dollar terms in 2026. South Korea’s Kospi has rallied 62 per cent. Japan’s Nikkei has gained 18 per cent. Even China’s Shanghai Composite is up 7 per cent. India’s Sensex and Nifty, by contrast, have fallen 13–14 per cent. If global factors were the sole explanation, the exit would be from all emerging markets equally. It is not. Capital is leaving India specifically — and rotating toward markets that offer better returns, stronger innovation ecosystems, and less punitive tax treatment.

Emkay’s observation is devastating: for a foreign investor, the combination of India’s capital gains tax and currency depreciation means that even if the Indian market stays flat, they are losing money in dollar terms. In 2024, the Union Budget increased LTCG tax on equities from 10 per cent to 12.5 per cent and STCG from 15 per cent to 20 per cent. The government framed this as “rationalisation.” Foreign investors experienced it as a signal that India views their capital as a revenue source to be squeezed, not an asset to be nurtured. When you tax capital gains, impose STT, depreciate the currency, and offer no offset for currency losses, you are effectively telling global capital that it is not welcome.

Net FDI: The Productive Investment That’s Evaporating

The FII exit is the visible headline. The FDI picture is quieter but equally alarming. While gross FDI inflows rose 13 per cent to $50 billion in FY2024–25, net FDI has halved — because disinvestments (foreign companies pulling money out) have surged. Repatriation now accounts for 63.5 per cent of gross FDI, up from less than 1 per cent in the early 2000s. Indian outward FDI has nearly tripled in five years to $29.2 billion, meaning Indian companies themselves are investing abroad rather than at home. FDI in manufacturing has declined to just 12 per cent of total inflows — a damning verdict on the “Make in India” programme. Investments from technology leaders like the US, Germany, and the UK have declined. The composition of inflows is increasingly dominated by financial flows routed through Singapore and Mauritius, not productive greenfield investment.

The reasons are interlinked: regulatory complexity, unpredictable retrospective taxation, a “licence raj 2.0” of compliance requirements under GST and the new Income Tax Act, corruption in contract allocation that favours connected domestic players over foreign entrants, and a judicial system that takes decades to resolve commercial disputes. India, for all its growth narrative, is increasingly a market that global investors find easier to trade from a distance than to build factories in.

III. The Falling Rupee: From INR 83 to INR 97 in Eighteen Months

Asia’s Worst-Performing Currency — and the Structural Rot Behind ItThe Indian rupee has depreciated approximately 7 per cent in calendar year 2026 alone, falling from near INR 89 per US dollar at the start of the year to a record intraday low of INR 96.95 on 20 May 2026. It is the worst-performing currency in Asia — worse than the Indonesian rupiah, the Thai baht, the Malaysian ringgit, or even the Pakistani rupee against which it has fallen nearly 12 per cent since mid-2025. The full-year depreciation rate of 2026 has already exceeded the total depreciation for the entirety of 2025 in just five months. Analysts now openly discuss the possibility of the rupee touching INR 100 to the dollar.

The proximate causes are well documented: the West Asia conflict pushing crude above $110 per barrel, FPI outflows of over INR 2 lakh crore creating massive dollar demand, elevated US bond yields making dollar-denominated assets more attractive, and the RBI’s $103 billion intervention problem — the central bank has spent tens of billions defending the rupee, depleting reserves that took years to build.

But the structural causes run deeper. India imports 88 per cent of its crude oil. Its trade deficit is widening. Its current account is under strain. And the capital that is supposed to offset these structural deficits — FDI and FPI — is leaving, as documented above. A country that is structurally dependent on energy imports, that taxes its investors punitively, that imposes regulatory complexity on businesses, and that does not produce the kind of high-value innovation that attracts patient capital, will always have a weak currency. The rupee’s decline is not a temporary shock. It is a verdict on the economy’s underlying competitiveness.

Rupee at ~INR 85 per dollar. FPIs begin sustained selling. Currency begins steady decline that would total 6% for the year — the worst performance in Asia.

Rupee breaches INR 90. Iran crisis escalates. Crude crosses $100/barrel. RBI begins aggressive intervention, spending billions in reserves.

Rupee crosses INR 95 for the first time. FPIs pull out over $11 billion in March alone — sharpest monthly outflow since October 2024. Crude at $102/barrel.

Rupee touches all-time intraday low of INR 96.95. Closes at INR 96.86. Total 2026 depreciation: 7.04%. Analysts warn INR 100 is possible if current pace continues.

Innovation Deficit: The Root Cause Nobody Talks About

Taiwan’s currency and stock market have surged because TSMC and its semiconductor ecosystem represent irreplaceable technological value. South Korea has Samsung and its AI chip investments. Japan has its robotics and automotive innovation clusters. What does India export that the world cannot get elsewhere at a better price? IT services — a sector that is now under pressure from AI automation and H-1B visa fee hikes. Generic pharmaceuticals — where margins are thin and competition from China is intensifying. Textiles — where Bangladesh and Vietnam are more competitive.

The Modi government’s answer to this innovation deficit has been “Make in India,” “Startup India,” and production-linked incentive schemes. After a decade, India’s manufacturing share of GDP has barely moved. The PLI schemes have disproportionately benefited large, connected conglomerates — the Tatas, the Adanis, the Ambanis — rather than creating a broad-based innovation ecosystem. Venture capital funding has dried up. Startups are shutting down or relocating to Dubai and Singapore. The brightest Indian engineers and scientists continue to leave for the US and Europe, not because they lack patriotism, but because the domestic environment — the taxation, the corruption, the regulatory maze, the institutional decay — makes it irrational to stay.

A falling rupee is the market’s summary judgment on all of this. It says: this economy does not produce enough of what the world values to sustain the currency at which it wishes to trade. No amount of RBI intervention can override that fundamental signal.

IV. Crony Capitalism: Who Actually Benefits From “Reform”

Tax Holidays for Billionaires, Tax Terror for the SalariedThe cruel irony of the Modi government’s economic management is that it uses the language of reform — “ease of doing business,” “minimum government, maximum governance,” “Viksit Bharat” — while presiding over a system that systematically directs public resources, tax breaks, and regulatory favours toward a handful of politically connected conglomerates.

Corporate tax was slashed to 22 per cent in 2019, costing the exchequer an estimated INR 1.45 lakh crore annually. The stated rationale was to attract investment and stimulate growth. The actual result: the largest beneficiaries were already-profitable firms. India’s investment-to-GDP ratio did not meaningfully improve. Manufacturing’s share of GDP remained stagnant. But corporate profits hit record highs, executive compensation soared, and the stock market — until the recent correction — masked the economy’s underlying weakness with an asset-price boom that benefited the top 5 per cent of the population.

Meanwhile, the same government that cut corporate tax introduced the angel tax on startup funding (since partially rolled back after years of damage), raised LTCG and STCG rates, maintained STT, and kept GST at 18 per cent on most services. The message is unmistakable: if you are big and connected, you receive tax cuts. If you are small, salaried, or just starting out, you receive tax demands.

The government’s fiscal giveaways before elections — the INR 1 lakh crore income tax concession before the Delhi elections in February 2025, the “double Diwali” GST bonanza before the Bihar polls, announced by the Prime Minister himself — reveal the cynicism most clearly. These are not structural reforms. They are transactional vote purchases, funded by the same middle-class taxpayer who is squeezed the rest of the year. As the Deccan Herald’s analysis noted, the two tax giveaways of 2025 punched a INR 3 trillion hole in the government’s revenues. And who will pay for that hole? Not the billionaires. Not the politicians. The salaried taxpayer, through future cess increases, service charges, and indirect tax hikes that are already being planned.

V. Licence Raj 2.0: The Compliance Nightmare That Drives Away Investment

GST Returns, Tax Notices, and the Bureaucratic LabyrinthThe Modi government promised to dismantle the licence raj. What it has built, in its place, is a digital compliance raj that is in some ways worse — because it combines the old bureaucratic instincts of the Indian state with the surveillance capabilities of modern technology. GST, introduced in 2017 as a transformative simplification, has become a labyrinth of multiple slabs, classification disputes, input tax credit mismatches, and a compliance architecture that requires small businesses to file monthly and quarterly returns on a portal that is infamous for crashes and glitches. The number of GST notices and demands issued by tax authorities has risen dramatically, with businesses spending more time complying with the tax system than growing their enterprises.

Income tax enforcement has become increasingly aggressive. Tax demands are issued based on algorithm-driven assessments that frequently produce absurd results. The tax terrorism extends to startups being slapped with angel tax notices on legitimate funding rounds, to salaried employees receiving demands for minor discrepancies in TDS, and to small business owners being subjected to surveys and raids that cost them weeks of productive time, only to result in no additional liability. The new Income Tax Act of 2025, touted as a simplification, is 622 pages long — compared to the 298 pages of the original 1961 Act.

For foreign investors and multinational corporations, the regulatory environment is even more treacherous. India’s history of retrospective taxation — the infamous Vodafone case, the Cairn Energy dispute — has left a permanent scar on investor confidence. Disputes take years to resolve in Indian courts. Contract enforcement is weak. Land acquisition is a political minefield. And the “ease of doing business” rankings that the government celebrates are based on reform of rules on paper, not on the lived experience of someone actually trying to open a factory, hire workers, and navigate the labyrinth of central, state, and local approvals.

VI. A System Designed to Fail the Citizen

Let us state plainly what the data shows. India’s honest, salaried, middle-class taxpayer — the software engineer in Bengaluru, the teacher in Pune, the accountant in Delhi, the bank officer in Chennai — pays more in cumulative taxation than their counterpart in most developed countries, while receiving public services that would shame a developing one. They watch as billionaires enjoy tax holidays, as agricultural income remains untaxed regardless of scale, as politicians’ wealth multiplies without scrutiny, and as the government takes credit for “tax reforms” that are either pre-election giveaways or repackaged extractions.

The foreign investor, looking at this system from the outside, sees a punitive capital gains tax, a depreciating currency that erodes dollar returns, regulatory unpredictability, and a market dominated by crony conglomerates. So they leave. Over INR 2 lakh crore gone in four months. Foreign holding at a 14-year low. The rupee at a record low of nearly INR 97 to the dollar — the worst-performing currency in Asia.

The entrepreneur looking to build something new in India sees a compliance nightmare, a tax system that treats early-stage funding as suspicious income, a market where government contracts flow to politically connected firms, and a regulatory environment where innovation is stifled by the very agencies meant to promote it. So they relocate to Dubai, to Singapore, to the United States — taking their talent, their ideas, and their potential tax revenue with them. A Lok Sabha question in February 2026 explicitly asked whether multiple taxation is compelling citizens to migrate abroad. The Finance Minister’s answer was to cite the tax-to-GDP ratio. The citizens, voting with their feet and their passports, have given a different answer.

Nirmala Sitharaman’s Finance Ministry has overseen the most sustained squeeze of the Indian middle class since economic liberalisation. Under the rhetoric of “Viksit Bharat” and “Amrit Kaal,” it has built a system where the honest pay the most, the connected pay the least, the foreign investor is penalised for participating, the domestic entrepreneur is punished for innovating, and the only guaranteed winners are the bureaucrats who administer the maze, the politicians who exempt themselves from it, and the billionaires whose empires grow precisely because the maze exists — because in India, complexity is not a bug. It is the product. It is how the powerful extract from the powerless, year after year, budget after budget, cess after cess, until the middle class is not squeezed but ground into dust.